One of the million-dollar questions, the one everyone wants answered when we talk about investing, is how to achieve recurring returns in the stock market without suffering too much.

In recent years, institutional investors have employed a new approach to Equity portfolio construction: factor-based investing. This increasingly popular approach lies between passive and active investing, allowing investors to target specific risk factors as well as market beta.

Factors are the primary market drivers of Equity returns. Only a few set of rewarded factors are backed by academic consensus:

- Quality: Businesses with strong economics. Average of trailing 12-month Return on Invested Capital (ROIC) and Return on Equity (ROE) and Interest Coverage Ratio

- Momentum: Companies already doing well in the market. Average of the trailing 6 and 12-month total returns

- Low Volatility: Stocks that show resilience. Average of the trailing 6 and 12-month standard deviation.

- Value: Attractive opportunities at sensible prices. Average of trailing 12-month EBITDA to Price and Revenue to Price.

So the aim is to find a systematic approach designed to invest in companies with the right balance of strength, trend, stability and price

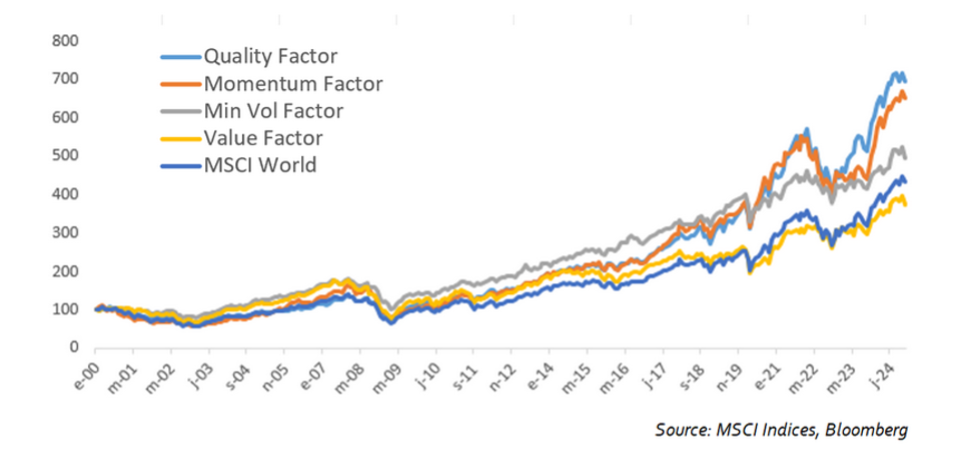

In fact, the best factor combination (Absolute Performance, Sharpe Ratio & Maximum Drawdown) since the launch of real pure factor investing strategies (Jan 1999) has not been constant. World factor performance has been impressive vs. MSCI World but quite divergent as we can see in the following graph:

The way to achieve capital growth over the long term should be investing in a selection of shares in leading global companies with enduring competitive advantages and a long runway of growth. This means investing in high ranked companies in terms of profitability (quality), value, good momentum and low volatility.

The most advaced models in Asset Management try to provide long-term capital growth through global and dynamic equity portfolios. Combining factors through a multi-factor allocation reduces the variability in performance through diversification and results in long-term historical outperformance. These models use differents types of dynamic approaches by adapting factor allocations to extract the benefits from the diversification effects of a multi-factor equity strategy.

“The most advaced models in Asset Management try to provide long-term capital growth through global and dynamic equity portfolios. Combining factors through a multi-factor allocation reduces the variability in performance through diversification and results in long-term historical outperformance.”

Also, most of these new products, and in accordance with article 8 of SFDR, promote environmental or social characteristics.

One of the most successful models comes from a 2018 MSCI paper, called Adaptive Multi-Factor Allocation (Hitendra D. Varsani, Vipul Jain).

How does it work and how can we turn it into an investable product? Each quarter, for the 3 main geographic areas, that represent 85% of the whole world equity market (USA, Europe and Japan), we choose those stocks with the highest 4 factors combination depending on:

- The macro cycle, measured by known economic indicators. Theory suggests that systematic factor returns should be linked to the changing economic/business conditions

- The own 4 factors momentum. Relatively few studies on adaptive factor allocation have considered the momentum effect on factors themselves, but it certainly exists.

- The market sentiment (risk On/Off), measured by credit spreads and volatility curves. Market volatility has significant power to forecast payoffs.

The rebalancing is quarterly made in the 3 geographic areas. The resulting porfolio is forced to be Sector Neutral against its index using an Equity Optimizer. What this really mean? Easy: we will have a world stock portfolio that will be almost identical in sector weighting to MSCI World but with a combination of factor-optimized stocks and therefore, a greater probability of success.

It seems simple once explained, but it clearly requires a great deal of technical skill and financial expertise.

In fact, for those trying to find the right way to become a Factor-Investor, there are already passive and active Factor UCITS Funds and ETFs in the market, some of them trying to represent a single factor but also multi-factor and even Factor Rotation products. As of early 2026, the most popular factor investing UCITS investment managers in Europe are dominated by large, established index fund providers, with iShares (BlackRock) leading the market, followed by Amundi, Xtrackers (DWS), and Invesco.

These managers offer popular “smart beta” or factor-based funds targeting value, momentum, quality, low-vol, and multi-factor strategies, predominantly using indices from MSCI or STOXX. At fLAB Funds, we’ve tried to play this game, and in March 2025, we launched fLAB Equity, which is really a summary of everything explained above. The results have been very good, although in these kinds of things, it’s better to be cautious and not let emotions control your mind and your portfolio.

Authors

Oscar Álvarez

Chairman

fLAB fUNDS

Search posts by topic

Advisory (7)

AI (5)

Alternative Investment (25)

Alternative investments (3)

AML (1)

Art (1)

Asset Management (29)

Banking (16)

Capital Markets (1)

Compliance (1)

Crypto-assets (3)

Digital Assets (3)

Digital banking (6)

Diversity (9)

EU (6)

Family Businesses (4)

Family Offices (2)

Fintech (10)

Fund distribution (27)

Governance (12)

HR (9)

ICT (1)

Independent Director (9)

Insurance (3)

Internationalization (1)

LATAM (9)

Legal (11)

Private Equity (4)

Real Estate (2)

Regulation (1)

Reinsurance (2)

RRHH (1)

Stock Market (1)

Sustainable Finance (23)

Tax (17)

Technology (6)

Transfer Pricing (2)

Trends (22)

Unit-linked life insurance (6)

Wealth Management (13)